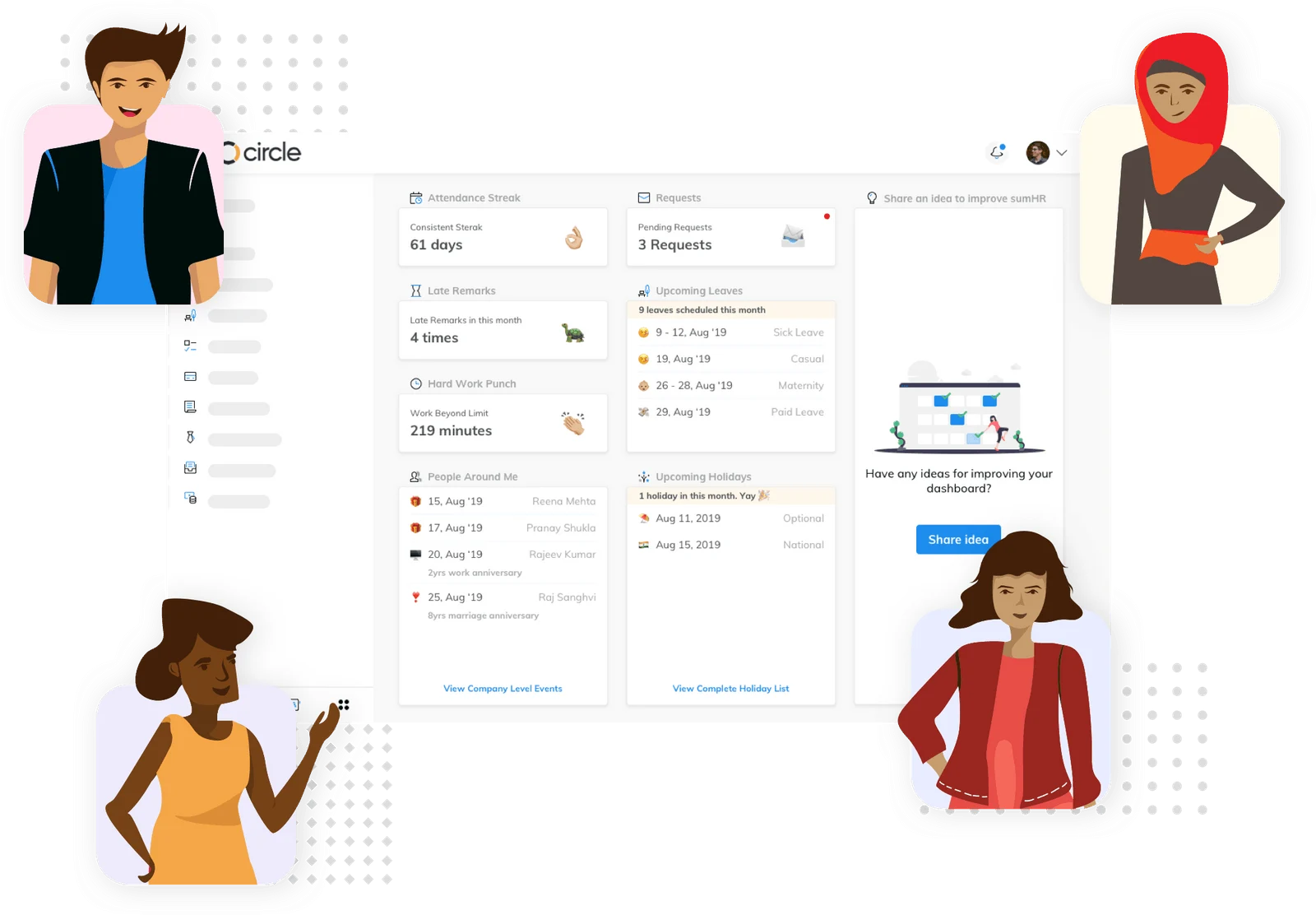

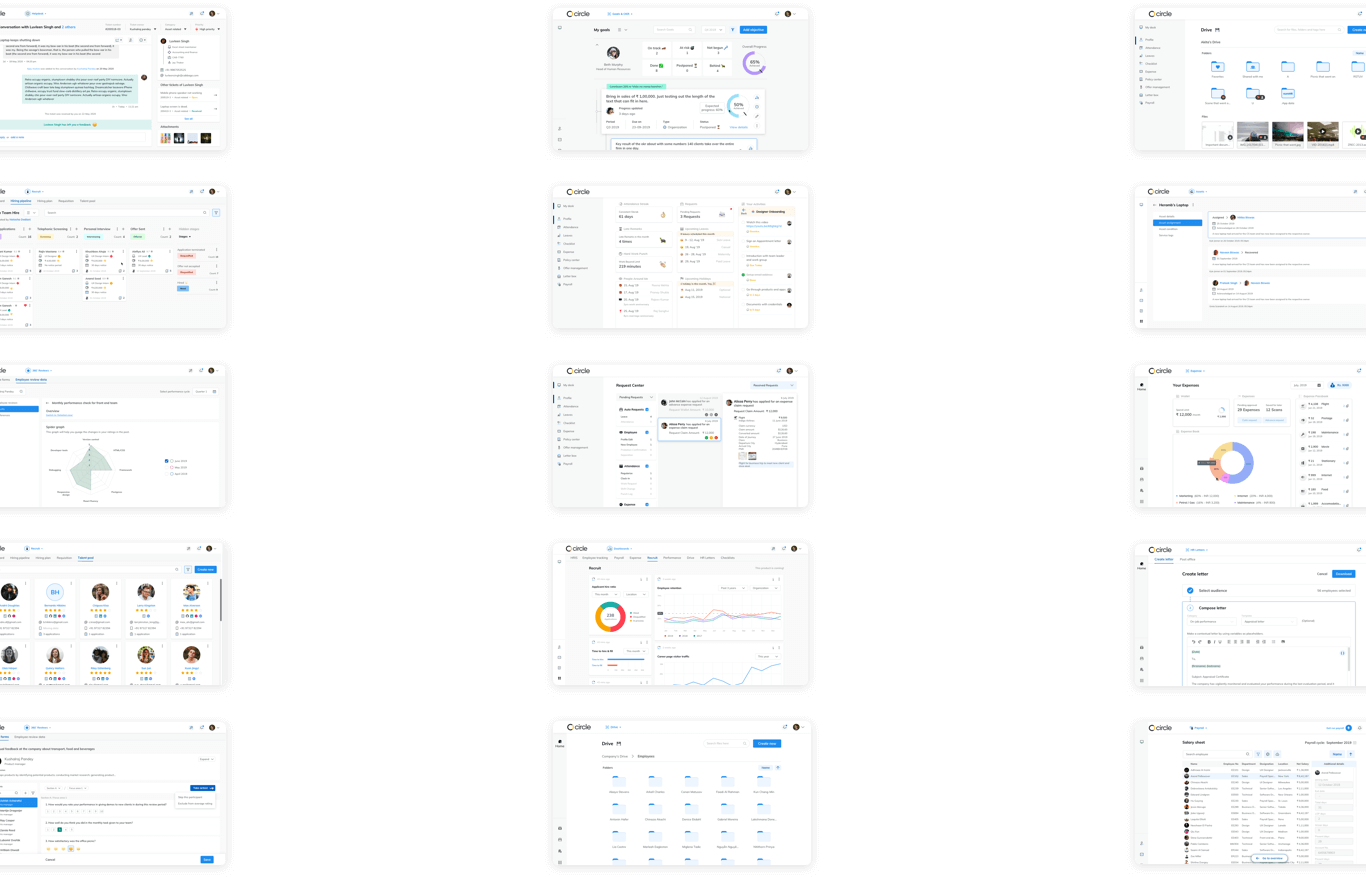

An HRIS packed with data points

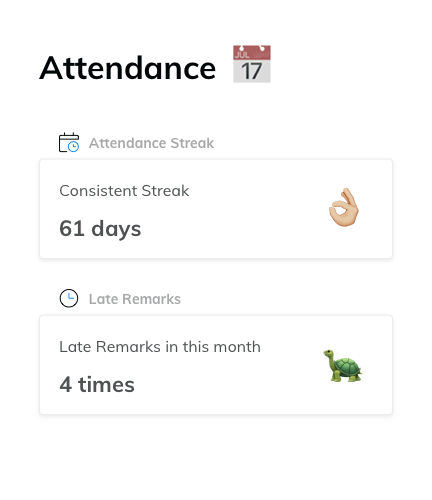

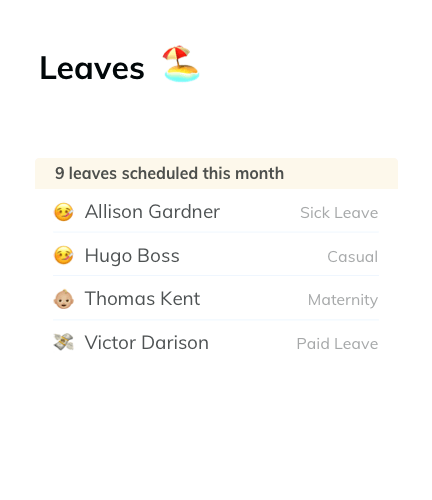

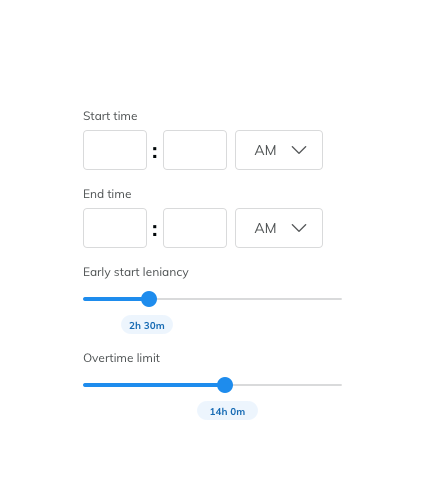

Biometric & GPS, plan shifts or leaves

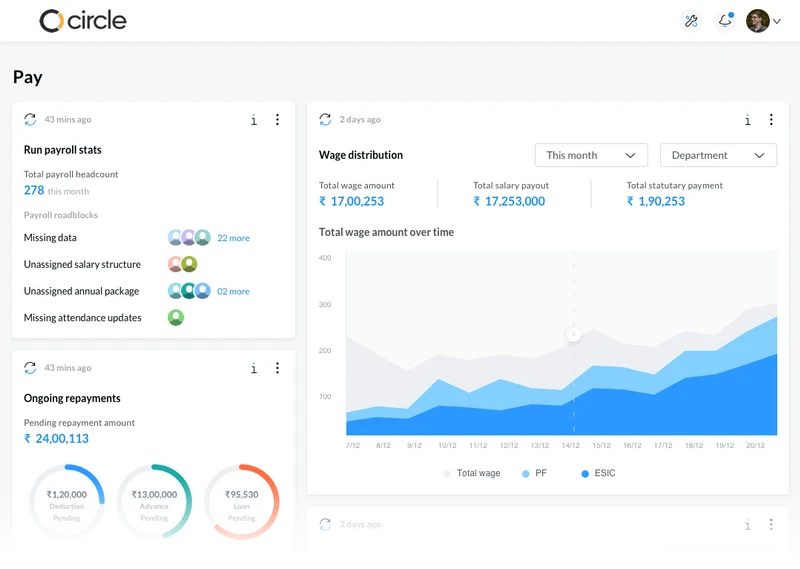

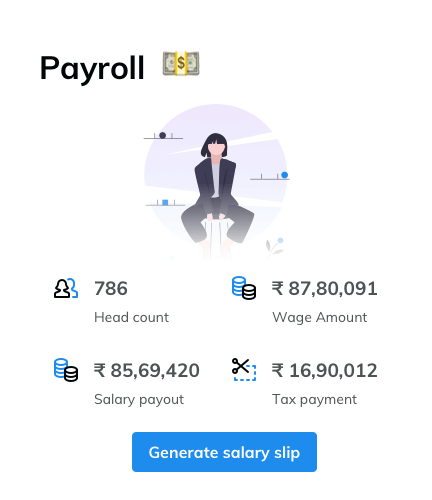

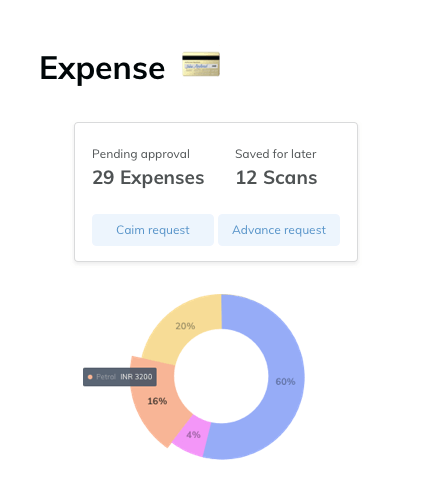

Do payroll in mins, keep claims in check

Generate letters, store docs & track assets

Onboarding & exit to an HR/IT helpdesk

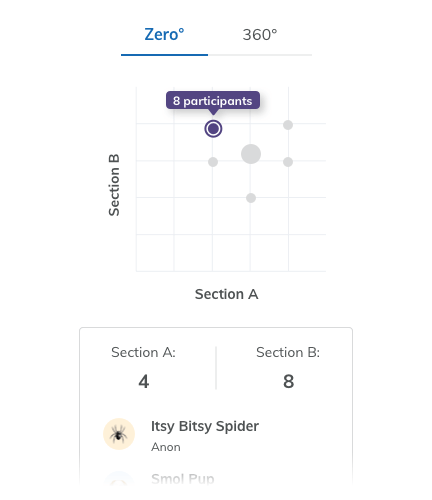

360°, competency maps & goal tracking

Career site, recruiter bot, & kanban ATS

Customers love us, for good reason

Happy conversations, timely resolutions

Who we are & why we have come together

Together we can do better & succeed faster

Our backers and cheerleaders

Whatever is on our mind, is on our blog